Canada’s Automotive Value Problem in Four Charts

The first Canadian patent for an electric vehicle was filed in 1893. The vehicle was known as the “Fethertstonhaugh” (say it three times fast, say it at all) and it debuted at the Dixon Carriage Works in downtown Toronto. The specs are charmingly tiny by today’s standards but genuinely futuristic for the time: about 15 mph, roughly 14–24 km of range.

Check out the image below to get a feel for it. The snap is of British engineer William Still demonstrating one of his early electrics in 1900. The Fetherstonhaugh had high seats for good visibility on muddy Canadian roads. Yeehaw!

More than a century later, Canada remains deeply tied to the auto sector, but our penchant for automotive patents has fallen off.

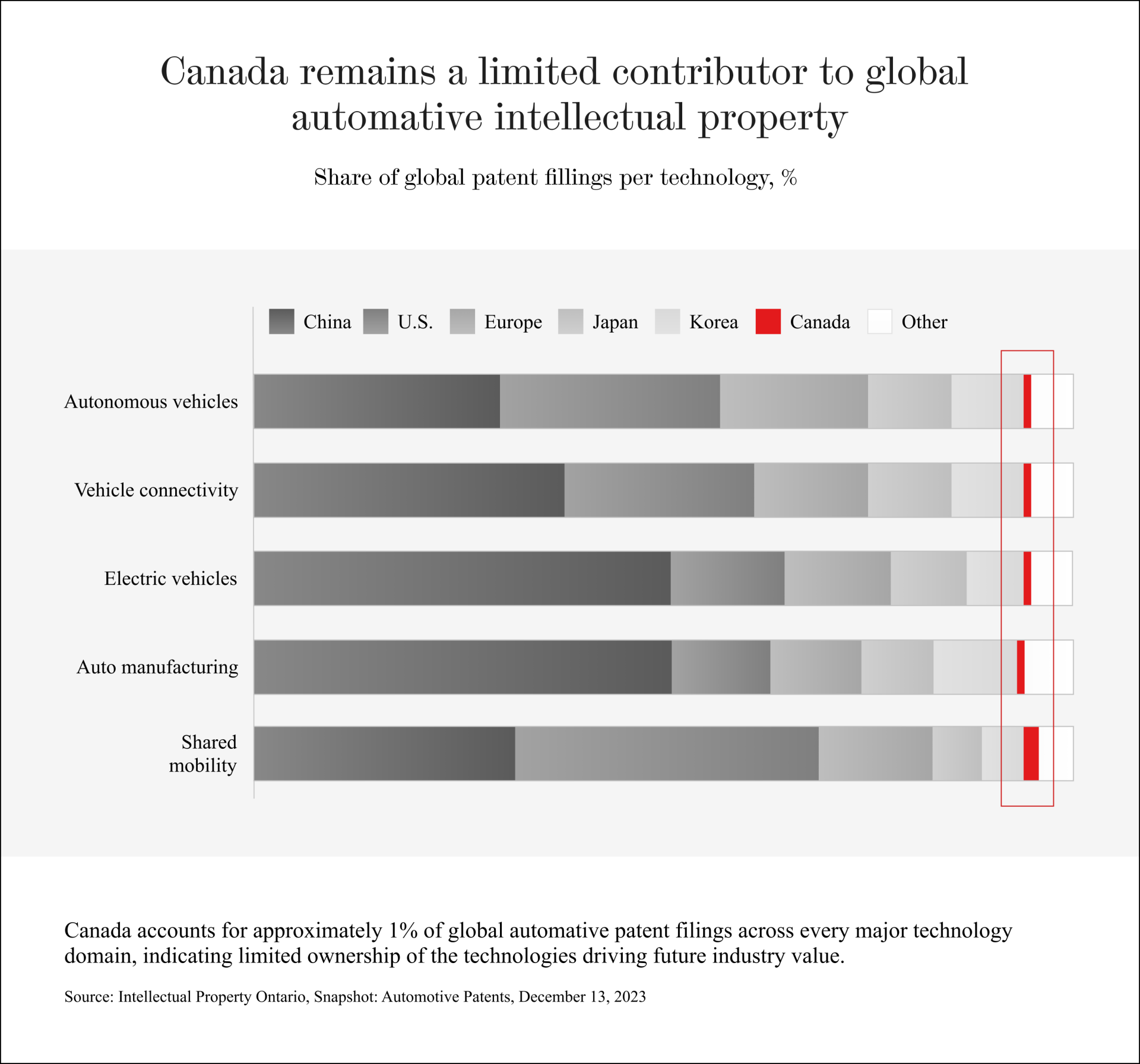

A 2023 automotive patent landscape report found that Canadian patent filings account for only about 0.9% of global automotive patent filings. A newer 2026 analysis puts Canada’s share of global automotive patent output at less than one-third of one percent.

For a really long time, the auto sector was understood through the logic of physical manufacturing at scale: who could make the most cars, most efficiently, at the lowest cost. Making stuff is just not the whole ball game of the new economy anymore.

The bulk of the economic value in the automotive sector is increasingly captured by software, engineering, data, batteries, autonomous systems, and intellectual property. In other words, the car is basically a rolling platform with cameras and sensors attached. And the companies that control the intangible assets which define the platform are able to capture a larger share of the revenue.

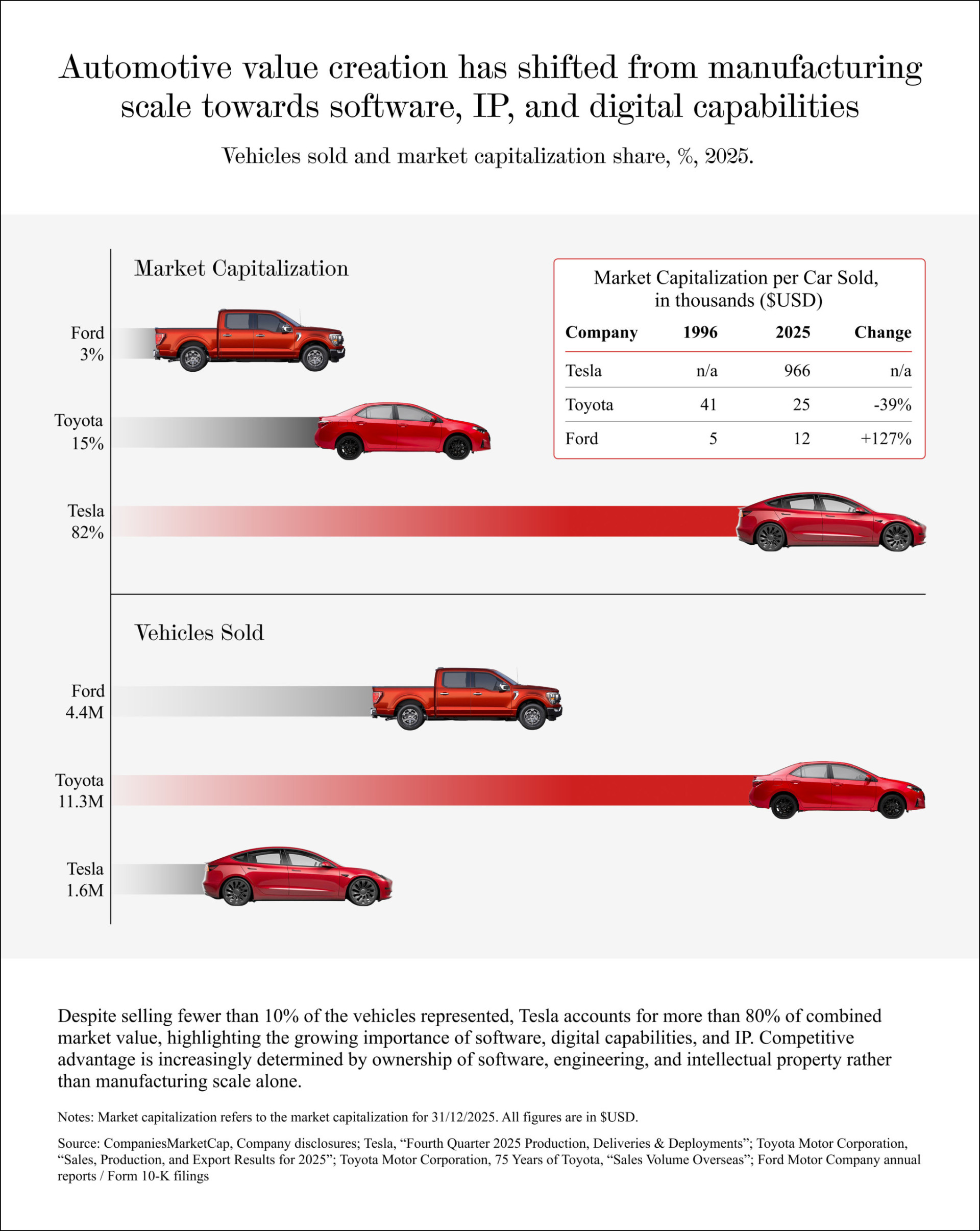

Tesla sells far fewer cars than Ford or Toyota, but investors value the company far more highly. Why? Partly because Tesla is viewed as a software and technology company, rather than an old-fashioned manufacturing company.

(Also, Tesla trades at a huge multiple because Elon Musk is a living, breathing meme stock, but enough said about that.)

You can see the discrepancy between Tesla and traditional automakers in this chart here:

This is one of those charts that looks absurd at first glance. Despite selling fewer than 10% of the vehicles represented, Tesla accounts for more than 80% of the combined market value of Tesla, Toyota, and Ford. Investors are valuing elements beyond the vehicle itself: software, data, batteries, charging infrastructure, brand, and the possibility of owning more of the technological stack around the car, like with autonomous vehicle technology.

So where does that leave Canada?

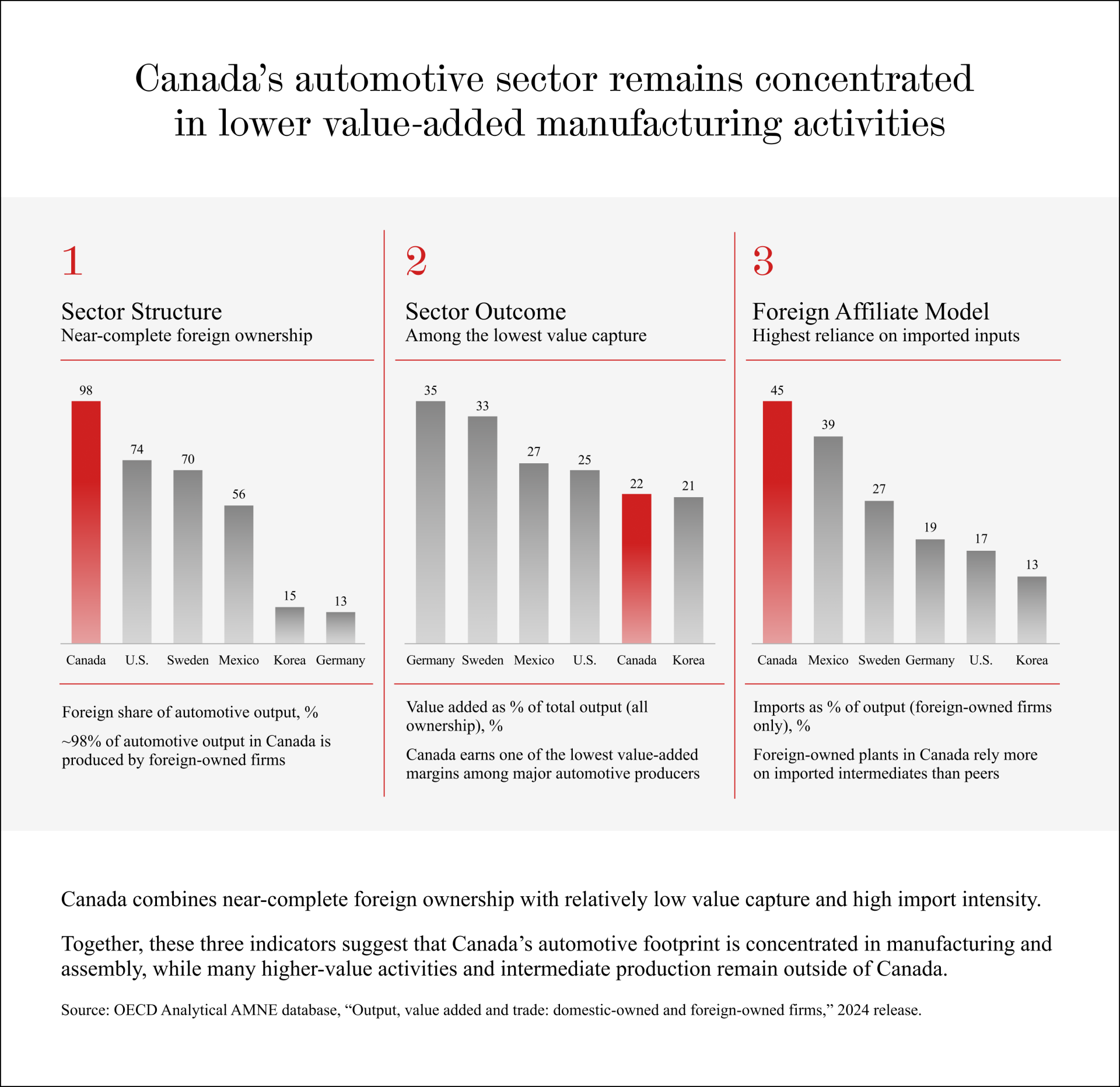

We are embedded in North American automotive supply chains. But looking more deeply at the structure of the sector gets a little uncomfortable.

Nearly all the automotive output in Canada is produced by foreign-owned firms. (Can you even name a Canadian car company or auto supplier?). Canada’s contributions to the supply chain also tend towards lower-value contributions, compared with several peer countries.

And foreign-owned plants in Canada rely heavily on imported inputs.

Put more simply: we are very good at hosting production, but we don’t control the most valuable pieces of it.

Of course jobs matter. But in the 21st century economy that’s dominated by software, data and intellectual property, it’s not all about jobs. More often, wealth-creation comes from who owns the intangible assets.

There is some good news here.

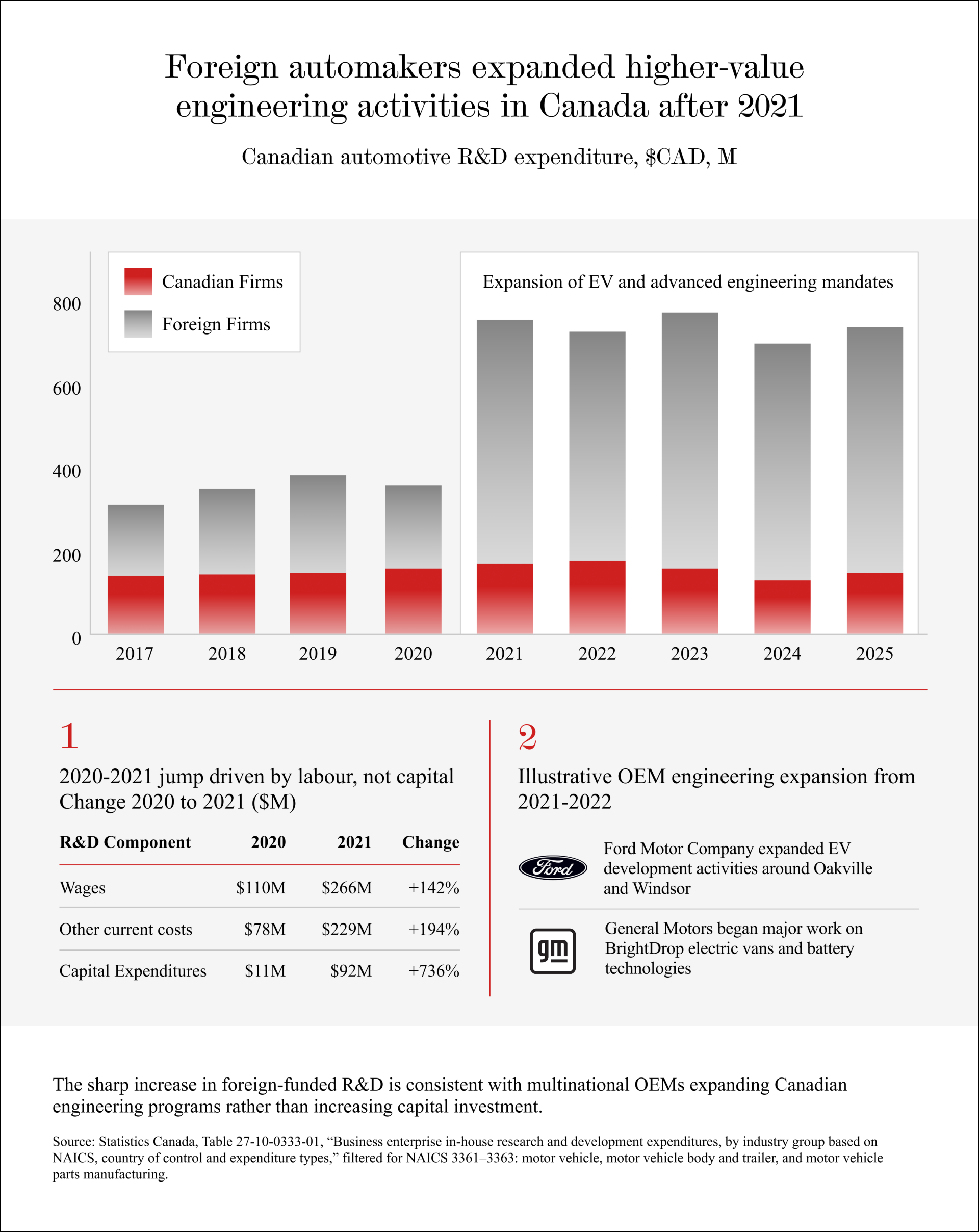

Foreign automakers have expanded higher-value engineering activities in Canada, especially after 2021. The jump in foreign-funded automotive R&D appears to be driven more by labour and engineering programs than by traditional capital investment alone.

That means Canada is not only being used as a place to bolt things together. There are real engineering mandates here. EV development, battery technologies, and advanced automotive programs are becoming part of Canada’s auto footprint.

But this raises the harder question: are we building Canadian capability, or simply supplying talent to foreign-owned strategies?

There is a big difference between doing sophisticated work in Canada and owning the intellectual property that sophisticated work creates.

This is where the picture gets much less comforting.

Canada remains a very small contributor to global automotive intellectual property. Across major technology domains — autonomous vehicles, vehicle connectivity, electric vehicles, auto manufacturing, and shared mobility — Canada accounts for roughly 1% of global automotive patent filings.

Patents are a useful signal of where technological ownership is accumulating. And right now, the major centres of automotive IP are China, the United States, Europe, Japan, and Korea.

Ultimately, the question we need to ask ourselves is this: What do we own? And are we actually capturing value from all of the economic activity that’s happening in the Canadian automotive sector?

That is the real lesson in these charts. Canada is in the automotive economy. But being in the industry is not the same as winning in it. To win, Canada needs to move from participation to ownership.

We dig into this in Episode Three of Cross Check, the YouTube-exclusive companion show to Gloves Off. In the corresponding episode of Gloves Off this week, you’ll hear about the Project Arrow concept car. We note that their operating system, DragonFireOS is from the Ottawa-based group Infotainment. Nice.

Watch Cross Check below, and keep these charts in mind.

Mapping Carney's Pivot

Canada has spent the last six months doing something we haven’t had to do in a generation: shopping for new relationships.

The deals are real and not the usual diplomatic pleasantries. The deals that Prime Minister Mark Carney is signing are creating new institutions and concrete commitments.

Canada has a trilateral technology and innovation partnership with India and Australia. We have a framework for arctic and space cooperation with Norway. We’ve entered into a sovereign technology alliance with Germany, and Norway might join that one too. And we’ve signed memorandums of understanding with Spain, UAE and Qatar, on AI infrastructure and emerging technologies.

A reorientation is coming together incrementally. But will it be enough?

This week, our friends at Gloves Off are looking at Canada’s international pivot. Host Stephen Marche asks: what cards do we actually hold against the global superpowers, and who should Canada be building strategic alliances with?

On the podcast, former Canadian diplomat Colin Roberson assesses the viability of a genuine third pole of power, while Antony Dworkin of the European Council on Foreign Relations explains how the EU has already started previewing what coordinated middle power leverage could look like.

To complement this episode, we’ve compiled our research into an interactive map of every significant agreement that Canada has signed since the crisis began.

You can sort it by type, by partner, and by whether the deal is forthcoming or already in place. Strategic partnerships, defence and security agreements, technology agreements, resource and energy cooperation: it’s all there.

The map only includes what’s real.

It paints a picture of Canada as a country that’s out hustling. The public debate hasn’t totally caught up with the speed of the pivot. pivoting faster than the public debate has totally caught up with.

A quick note on how we built it: we tracked every meeting between the Prime Minister and foreign ministers and scanned the associated PMO media releases. We did the same across key ministries (Defence, AI, ISED) and cross-referenced against news coverage from the Globe and Mail, CBC, Global News, and CTV. Our threshold for inclusion was strict: something had to be signed or a tangible new initiative had to be established. General commitments of cooperation, statements of intent, or expressions of shared values didn’t make the cut.

We’d love your feedback. Is an agreement something missing? Is something incorrect? Should something be removed? Provide insights through this google form.

We’ll also be adding new deals as they happen.

Subscribe to